Balance in the basket

Private labels and premium brands grow side by side across the region

The average number of brands present in Latin Americans’ shopping baskets has been increasing year after year. In 2023, there were 87; by 2025, that number had risen to 89. This shows that the intentional shopper is not merely looking to saving money but to balancing their shopping portfolio.

Within this context, two poles stand out. Economy and private-label brands each gained 0.4 percentage points in value share. At the opposite end, premium options rose by 1.4 percentage points, reaching 21% of total value in the region. The polarization becomes clear when we look at units purchased: Latin Americans are buying more premium items (+3), economy (+2) and private-label (+7), while reducing their choice of mainstream (–7) brands.

The choice of the pack size is also part of the intentional shopper’s value equation. Smaller formats play an essential role: they make premium and private-label brands more accessible, lower the entry barrier, and encourage trial. Larger sizes, on the other hand, gain strength within economy options, allowing greater savings per unit.

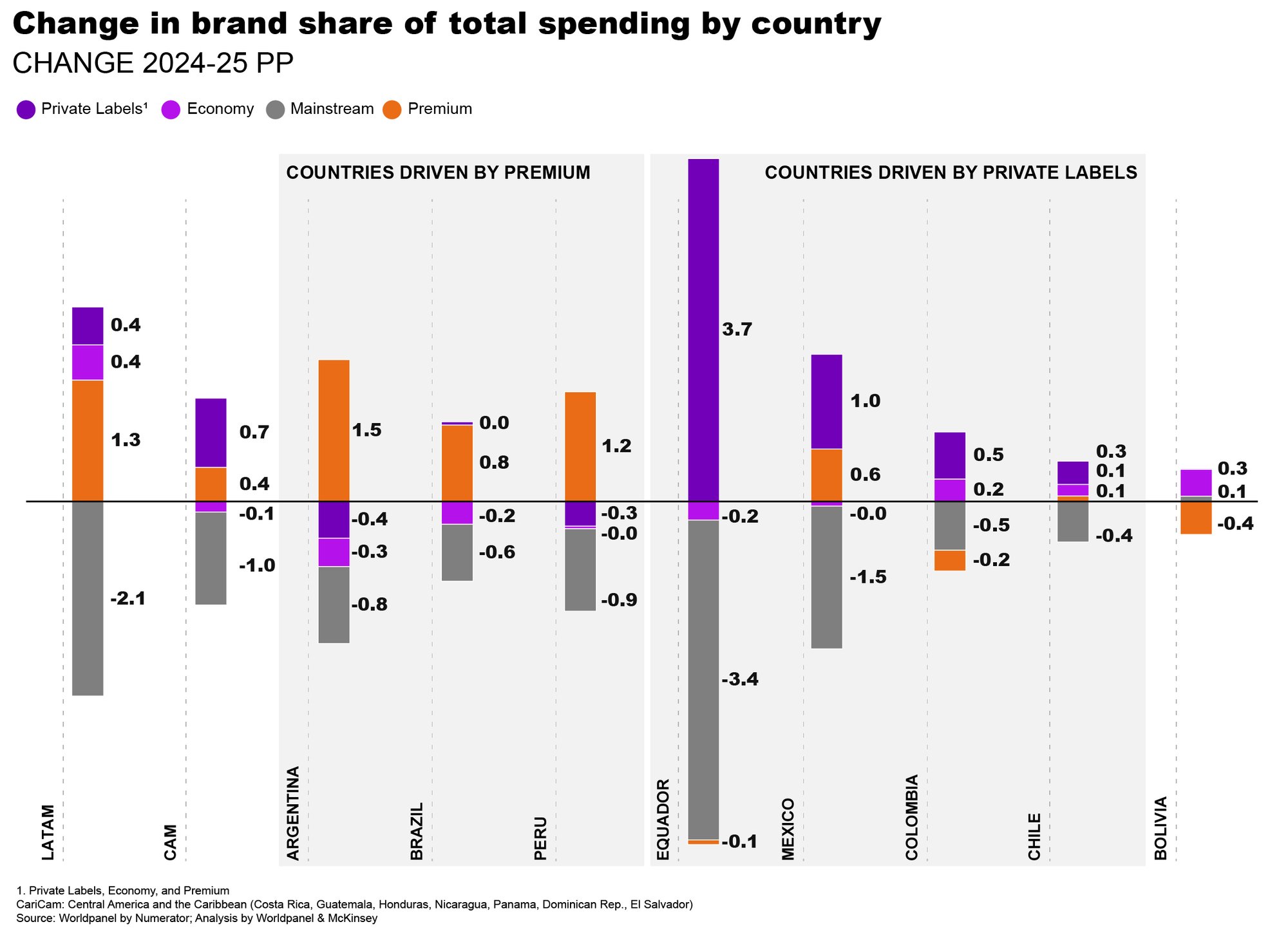

It is also worth highlighting that the advance of both premium and private-label brands extends across different categories — from dairy to household cleaning products — though with distinct dynamics in each country. Argentina, Peru, and Brazil are driving the rise of premium, with these brands gaining 2%, 1.3% and 1% in value share, respectively. In turn, Ecuador, Mexico, and Colombia see private labels as their main growth engine, boosted by the expansion of discount stores in these markets.

At the same time, the channel structure in the region continues to modernize. The traditional format, although still relevant, now accounts for 38% of the total spend, losing two percentage points in a year.

This space is being taken over by more structured formats — especially discount and cash-and-carry stores — which grew by one percentage point, reaching a 24% share.