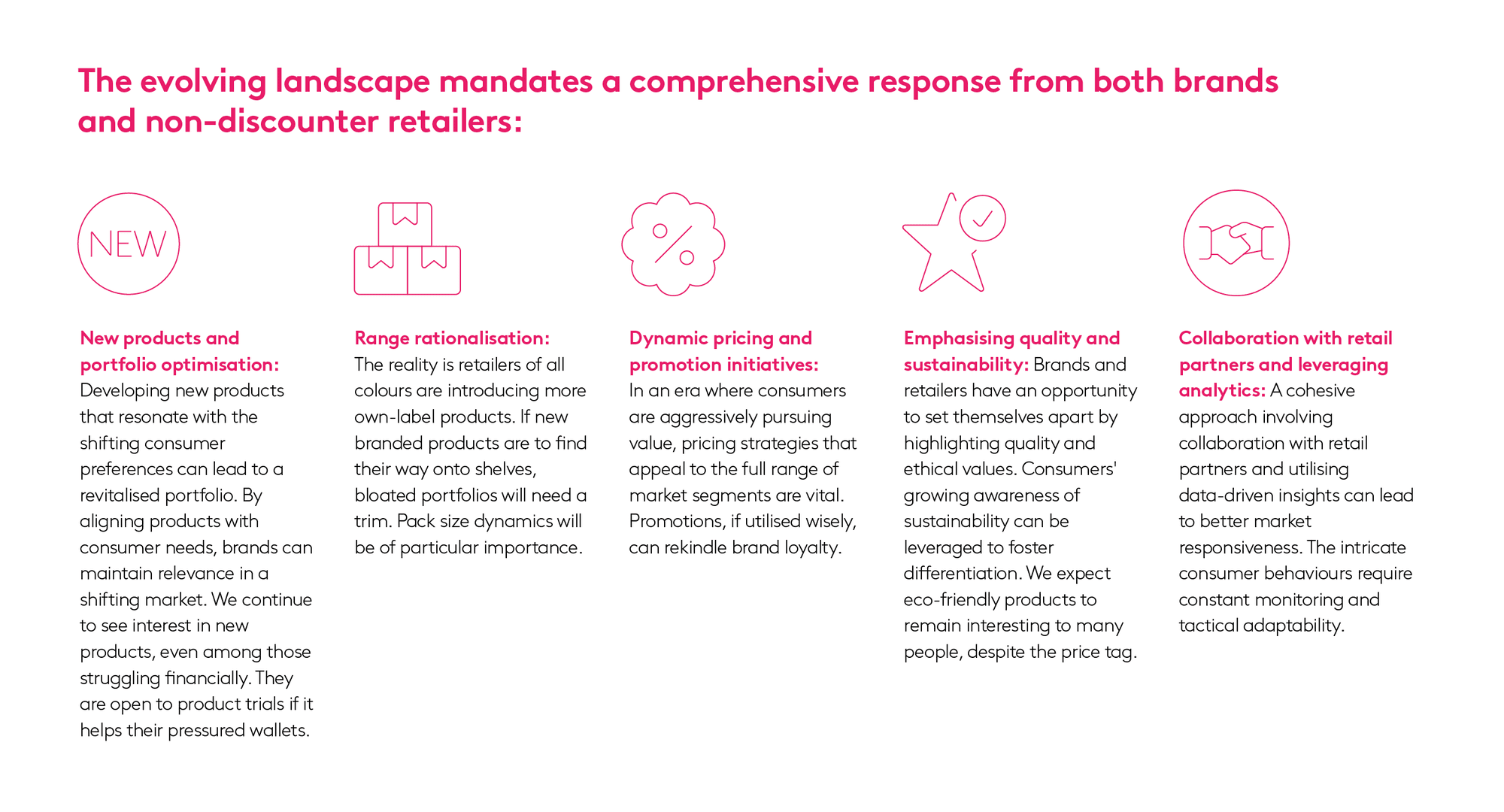

Brands in the balance

The shopping shift costing millions

In the bustling aisles of British and Irish supermarkets, a quiet revolution is taking place.

Kantar Worldpanel's latest analysis uncovers a seismic shift: people are flocking to own-label products. Far from being a blip, this migration is redefining the market, and the sense of urgency for brands couldn't be clearer.

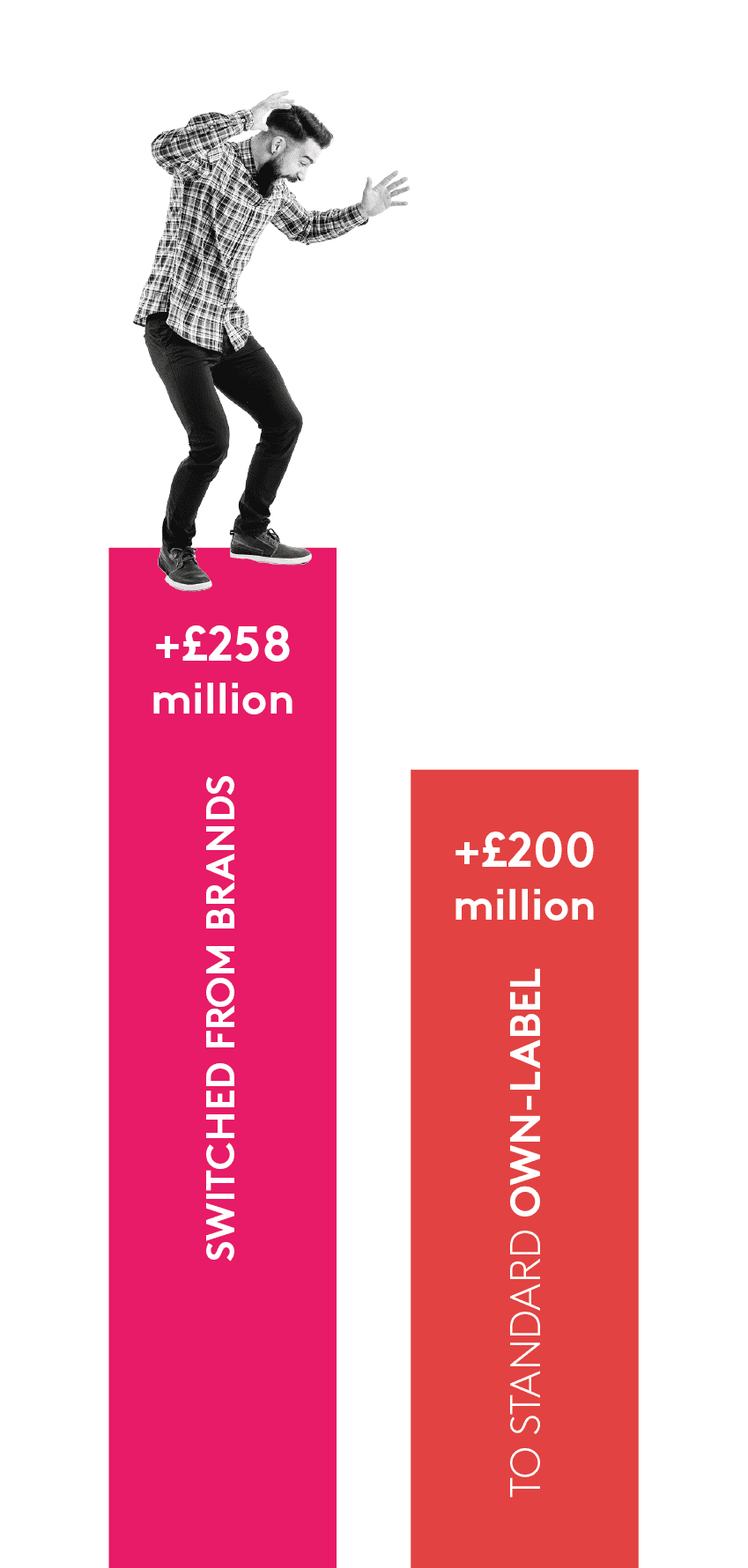

The facts speak for themselves: in a recent 12-week snapshot ending in June 2023, British shoppers spent over £258 million less on Fast Moving Consumer Goods (FMCG) brands, redirecting their pounds to own-label options. This wasn't a one-off; December 2022 saw an even more staggering dip, with own-label products capturing £331.6 million from their branded competitors. In Ireland, brands are seeing similar proportions of shifts from brands to own-label, particularly in value ranges. In the year ending July 2023, €17.1 million moved to own-label from brands.

In recent months, the haemorrhaging of consumer engagement with brands has shown small signs of abating, albeit with year-on-year losses still exceeding a not insignificant £200 million. This could be the market's early response to a deceleration in inflation, a factor that has traditionally inhibited consumer spending. Alternatively, we can’t preclude the effects of an emerging ramp-up in promotional spending to arrest the brand exodus.

But what's behind this shift in consumer behaviour, and how can brands respond? The finger of blame points squarely at the cost-of-living crisis, biting hard into spending power. Shoppers are hunting for value, and in the process, they're fuelling a surge towards own-label products. Of the £258 million switched from brands in the year-on-year snapshot for June, £200 million went to standard own-label. The balance went to the value and premium tiers of own-label, with a smaller portion going to loose products such as produce.

The sheer speed of this shift is also worth noting. In February 2022, the erosion in branded goods sales was a mere £16.87 million. Fast forward to February this year, and that figure exploded to £275.72 million.

Costly comparisons

While the rate of losses has slightly decelerated, own-label products and discounters continue to march forward at a steady pace. The story remains consistent even when widespread inflation, a particular concern in food products, is taken out of the equation. How do we know this? Because volume sales mirror the value sales trend of switching away from brands.

Of course, the real tension may lie in the specifics of this shift. The average price for a branded item over the last year in Britain has been £2.30 versus £1.65 for an own-label product. In Ireland, €3.29 vs €1.75. These comparisons, albeit at a high level, still illustrate the sort of savings that shoppers are craving. When we dig beneath the imbalance, we see ways for brands to navigate out of the price divide.

Deal or no deal?

Definitely, I miss the quality and trust.

Not a chance, own-label is all I need now.

Maybe, it would depend on the product.

I never switched; I've always bought branded.

One of those ways has been a move to higher levels of trade promotion. Promotions all but disappeared at the height of the Covid-19 pandemic when products in many categories were in short supply. Until recently, promotions had remained low, or even below pre-pandemic levels in many categories. But now, as brands race to hold their ground, the percentage of products sold on promotion, primarily supporting branded products, is growing year on year.

The promotional paradox: rewriting the rules of retail offers

Amidst the sweeping tide of own-label loyalty, there's another, less obvious narrative unfolding. In an era where every penny counts, it's counterintuitive that shoppers are distancing themselves from promotions, historically the battleground where brands have tried to win hearts, minds, and wallets.

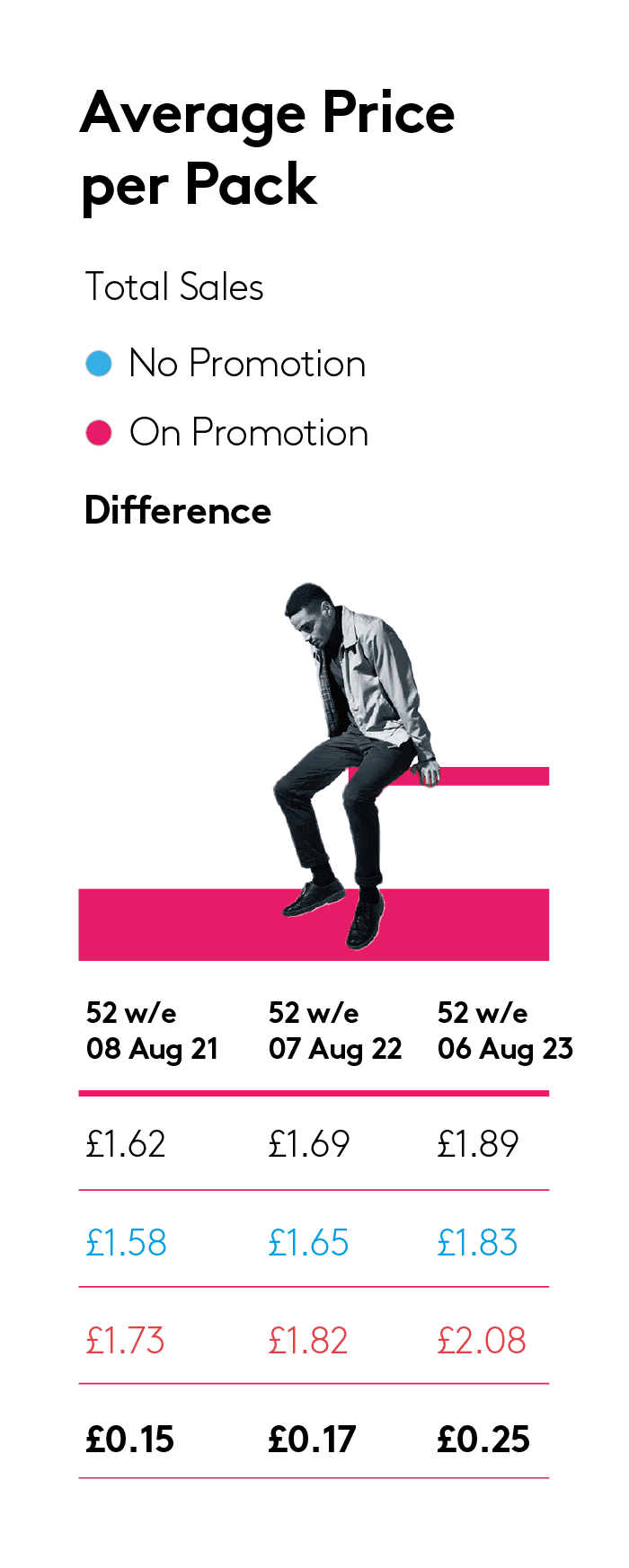

In a climate where "value" is the buzzword du jour, it would stand to reason that shoppers are drawn to promotions. However, the data paints an unexpected picture. The percentage of FMCG packs sold on promotion in Britain has dwindled from 28.3% in 2021 to 22.7% in 2023. Concurrently, the cost difference between promoted and non-promoted items has widened, with a £0.25 price gap in 2023 compared to £0.15 in 2021. Inflation has, unsurprisingly, played a part in this difference.

But here’s the more interesting part: the percentage of sales on promotion (the majority of which supports branded products) has — based on recent months — begun increasing year on year, against the long-term trend. This is a potential tailwind for brands if they can sustain the trend. Some categories have a better chance than others.

But for consumers, promotions might not be the fix for wallets they were hoping for. Promotions have been a mechanic which shoppers use to save money, which comes if they buy items at a cheaper price than they otherwise would have, or buy a higher proportion of their shopping mix on promotions.

But it turns out promoted products, on average, cost more, not less. Not only have items on promotion consistently cost more than those not on promotion for at least the past three years, but the price gap is widening. In other words, the cost of promoted items is rising more quickly than that of non-promoted items. While this trend is partially due to changes in the types of promotions available, the bottom line is that promoted items are becoming increasingly more expensive compared to their non-promoted counterparts. Given this reality, it's even more understandable why shoppers are moving away from brands to make their money go further.

If we dig deeper into this paradox, shoppers seem to be evolving, adopting a more discerning approach to their grocery buys. The complexity of modern promotional mechanics, from loyalty cards to 'Y for X' deals, has perhaps overwhelmed the average consumer. It may all be too much if they want something simple: value, even if there are trade-offs to be made.

Remember the 2008-2009 financial crisis? A similar trend occurred, where promotions were ramped up to entice consumers back into stores. It took over two years for the promotional landscape to return to some semblance of normality. History may be attempting to repeat itself. Recent data suggests a tentative return to this strategy, with a steady uptick in promotional activity over recent months. Whether this is a genuine reversal, or a temporary blip remains to be seen.

Our analytics at category and brand level are showing some interesting tensions: the market is oscillating between complexity and simplicity, forcing brands to choose their approach carefully.

Sophisticated promotional mechanics can attract a niche audience but may also deter the average shopper looking for straightforward value. On the flip side, a move towards everyday low pricing might restore value perceptions but risks diluting the sense of getting a 'deal.' Only 26% of spending is now on deals compared with 38% ten years ago.

As our world “unbrands” itself, the promotional landscape is becoming a complex maze that neither brands nor consumers seem particularly eager to aggressively navigate. The question looms large: can promotions, once the lifeblood of branded FMCG, adapt to a market where the rules are being rewritten?

Fickle future?

But what are the implications of these trends playing out amidst still high levels of inflation, especially as we head into another winter of high energy costs and little sign of a return to meaningfully lower mortgage rates? Will consumers return to brands they loved when their circumstances improve, or will they stick with the own-label products they turned to in tough times?

What's the forecast for the future? If the promotional trend persists, brands may find a foothold to claw back some losses, but it will require more than throwing budget back to promotion if profitability is to be found alongside a return in sales.

As consumer behaviour sways towards affordability, the business environment for consumer goods brands is charged with challenge and change. The tension between quality and cost, brand loyalty and price sensitivity, rages on. For brands to stay relevant and regain ground, they must understand the landscape, adapt their strategies, and perhaps most importantly, speak to the values and needs of today's discerning consumer.

This story of market shift isn't just a fleeting headline; it's an evolving narrative of economic pressures, consumer empowerment, and industry adaptation. For those who wish to explore the deeper implications and strategies for the future, the switching trend from brands to own-label is one of the essential starting points for recalibrating the compass.