Retail rupture

Discounters are redefining bargain shopping

The rise and rise of own-labels and discounters is more than just a blip on the retail radar; it's a seismic shift, signalling even more change in consumer behaviour. Amid a grim economic landscape, they are flourishing, offering quality, affordability, and accessibility.

Riding on these traits, discounters like Aldi and Lidl are also successfully breaking free from traditional discount shopping stereotypes. Discounters and own-label products were, of course, popular before, but their growth rate is on the rise.

Grocery inflation, though showing month-on-month declines recently, still sits at 12.2% in Britain and 11.5% in Ireland, as of early September. Prices are still up year-on-year across every supermarket shelf, but consumers will have been relieved to see the cost of some staple goods edging down compared with earlier in 2023.

British shoppers paid £1.50 for four pints of milk in July, down from £1.69 in March, while the average cost of a litre of sunflower oil is now £2.19, 22 pence less than in the spring. In Ireland shoppers spent €1.88 up 0.24 year-on-year on milk (price average per pack) and €1.88 up 0.24 year-on-year in cooking oils.

Amid these changes, the battle lines are being re-drawn to drive shoppers into stores with targeted pricing as the herding mechanism. The dairy aisle is now commonly being used as a loss leader to bring customers in-store in search of even small savings on staples like milk.

But the clear winners in this environment are the major discounters – Aldi and Lidl.

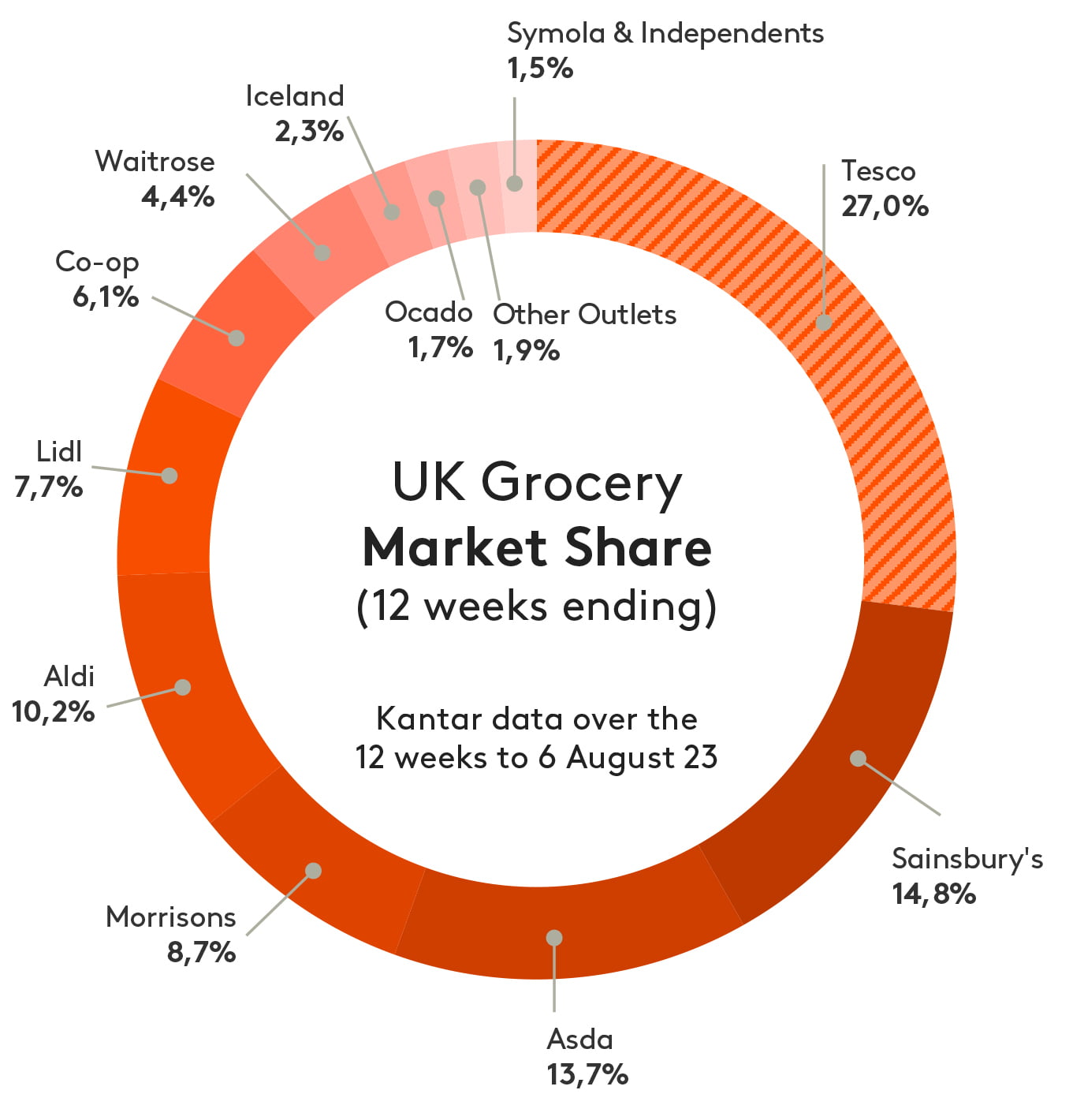

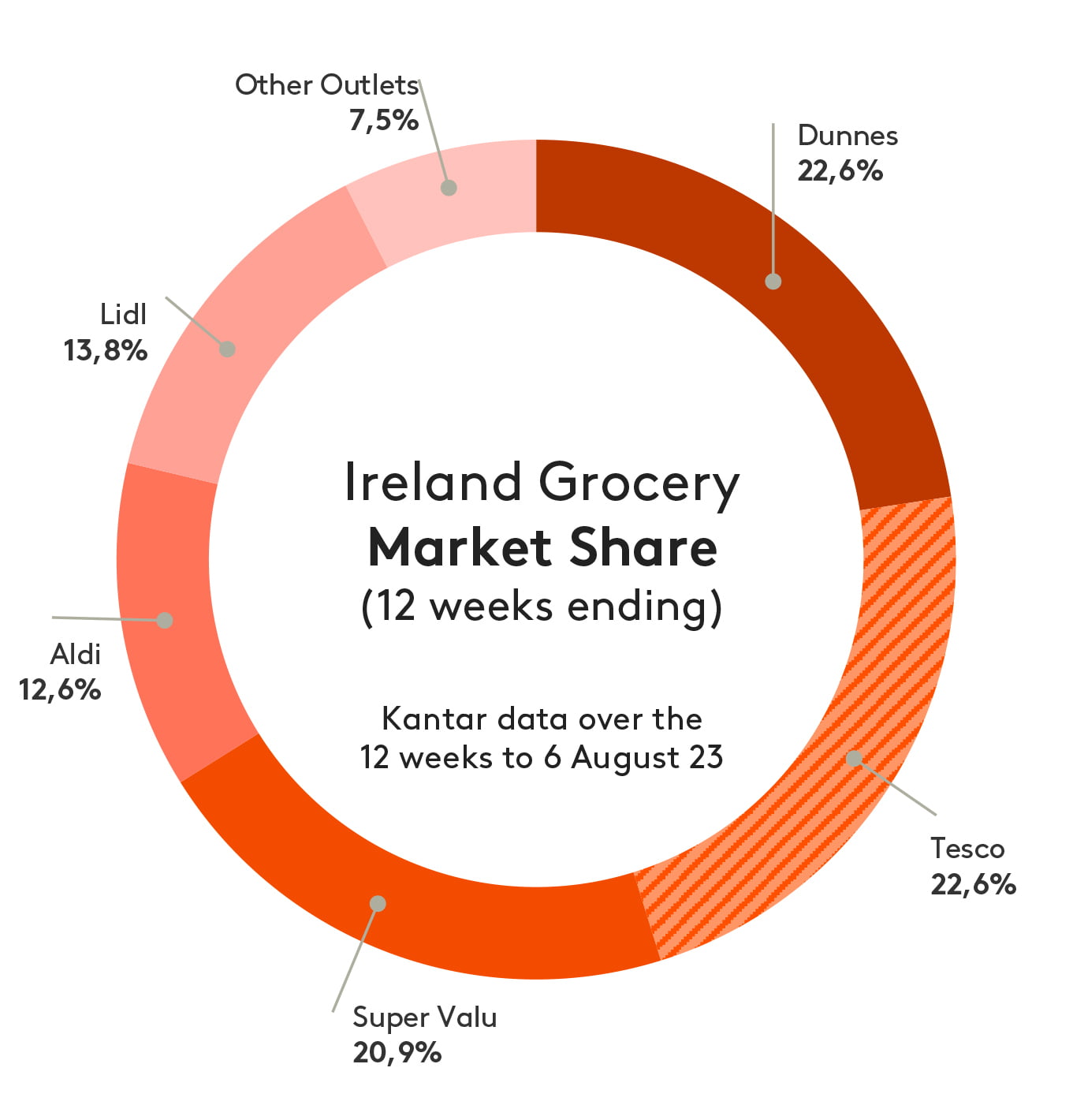

In Britain, Aldi has been the fastest growing retailer four months in a row, with sales increasing by 17.1% as of early September versus 2022. Between them, Aldi and Lidl now capture 17.7% of the market. The so-called traditional Big Four – Tesco, Sainsburys, Asda, and Morrisons – are generally seeing a rise in sales, but this is largely driven by inflationary increases not volume. In Ireland, the discounters are also continuing to build on a position of strength.

Of course, this pressure comes as Aldi and Lidl focus even more on the consumer hunt for value, breaking traditional stereotypes still associated by some with discount shopping. Their appeal isn't just limited to their prices, a driving attribute of the past. Their blend of variety, freshness, and locality is creating a powerful pull towards these stores. And their rollout of new stores and heavy advertising campaigns continue at pace. Expect them to double down on these actions.

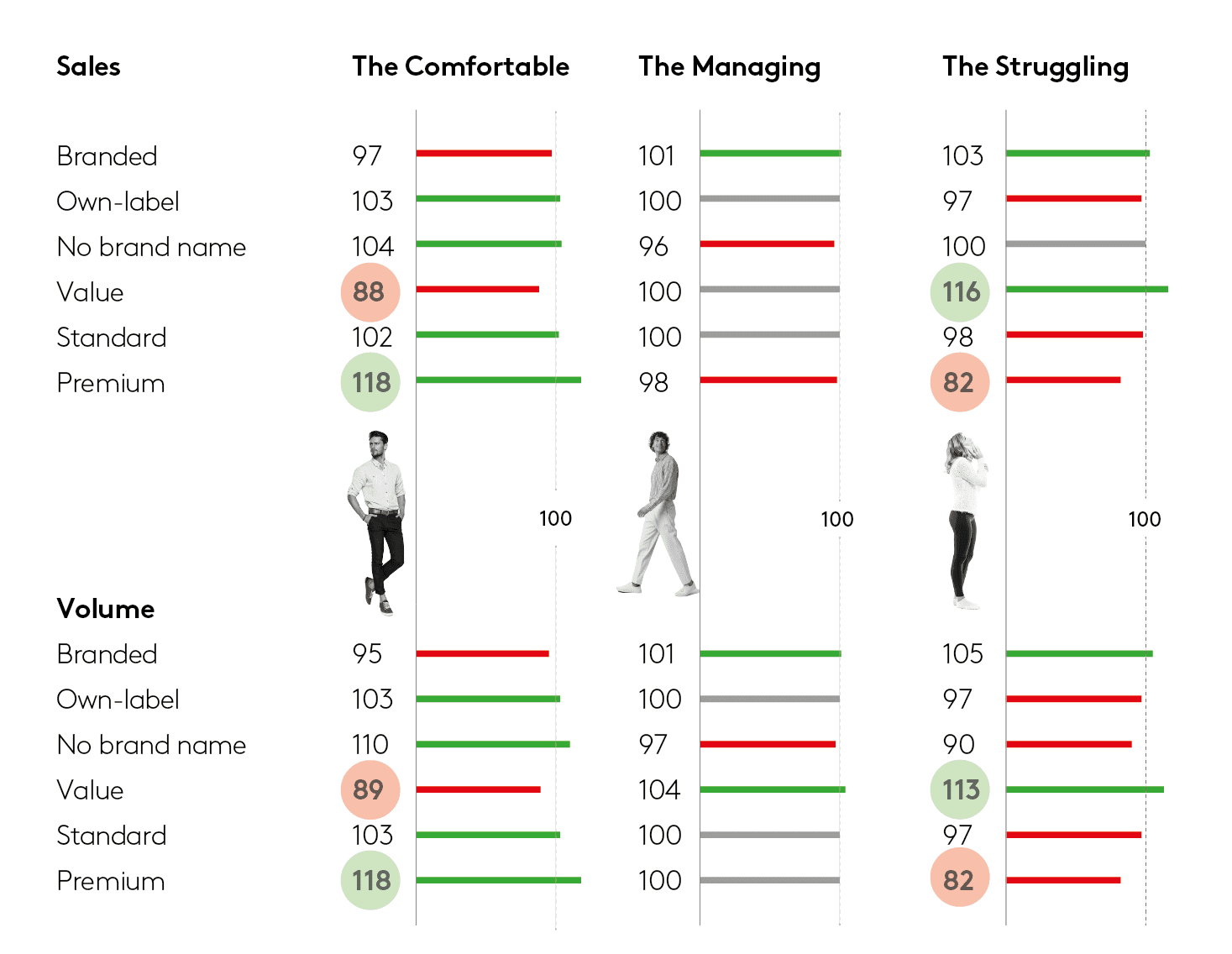

Although standard own-label items maintain a majority market share, the value and premium segments of retailer brands are gaining momentum. More and more consumers are exploring a diverse range of own-label alternatives, thus improving the overall standing of own-label products.

“Comfortable” consumers are playing a role here. It is worth noting that consumers who consider themselves in a comfortable financial position are buying more own-label, albeit at the premium end of the spectrum. As counter-intuitive as it may seem, those struggling are not more likely to buy more own-label than the comfortable. Consequently, own-label is strong at both ends (value vs. premium) but the less affluent are typically already buying meaningful amounts of own-label, so bigger increases are less likely to occur.

Index in July 2023 of how each British consumer pressure group is spending on own-label and branded products on a value sales and volume sales basis:

Price pursuits

The numbers tell the story: in response to cost pressures, consumers are skirting higher prices by opting for more own-label goods.

The share of own-label products in the total market climbed from 49.7% in August 2021 to 51.9% in August 2023 across Britain. In Ireland, own-label share moved from 44.5% to 48.2% with the biggest rise coming from Lidl. This clear trend underscores a fundamental shopper quest for affordability in an increasingly expensive world.

The uptick in own-label products is evident across the board, but as the numbers show, Aldi and Lidl are proving particularly adept at leveraging this trend. These discounters, known for their low prices and own-label portfolios, have seen their percentage of own-label sales in Britain rise from 86.9% in August 2021 to 87.6% in August 2023.

Yet, this growth narrative for discounters hints at a contrasting — perhaps even sobering — storyline for other retailers.

The traditional British Big Four have increased their own-label sales, but lag behind in both capturing consumer spending share and matching the volume growth seen by Aldi and Lidl. They’ve watched their share of the own-label market erode and find themselves grappling with a puzzle of increasing complexity – how to compete effectively with the rising might – and store footprint – of discounters.

A. Yes, it’s the only thing holding me back.

No, I’ll still also do some online grocery shopping elsewhere.

I've already made the switch.

Yes, if they opened a store near me.

This tale of two sectors within the consumer goods industry underscores the power of economic pressures in shaping consumer behaviour. As the quest for affordability intensifies amidst ongoing inflation, Aldi and Lidl are responding. Other retailers, meanwhile, find themselves at a crossroads, compelled to reassess their strategies or risk losing more ground. Brands, as is often the case, find themselves stuck in the negotiating ground somewhere in the middle.