Dollars and sense

Purchase perspectives fuel shopper decisions

It may be obvious that shoppers are in search of value. But it’s more complicated than that. Their search is not just about finding the cheapest options but a careful balancing act of managing household finances and maintaining a desired standard of living.

An ongoing shift in household dynamics underscores the impact of the cost-of-living crisis. As of August 2023, the proportion of households identifying as struggling has risen by 2% since April 2022, accounting for 24% of households. Groceries, once a staple expense, have become a point of concern for two thirds of households across the three pressure groups, but sits at 91% among the struggling (very concerned or extremely concerned). The impact of this concern should not be underestimated, given these households represent £92 billion in annual grocery spending.

On the other hand, there are signs of optimism. While it’s still low, 15% of people expect their household finances to improve in the next year, up a point from May. By aligning their offerings with these shifting consumer sentiments, brands have an opportunity to foster deeper connections with consumers, build loyalty, and navigate this challenging economic landscape.

For brands, the key lies in striking a balance between perception and reality, and ensuring that brands cater to the true, changing needs of consumers.

It is essential to recognise that consumers are seeking more than just low-cost alternatives; they seek products and services that offer real, tangible value for their money. Perception can quickly become reality if a brand fails to position itself within this shopper mindset.

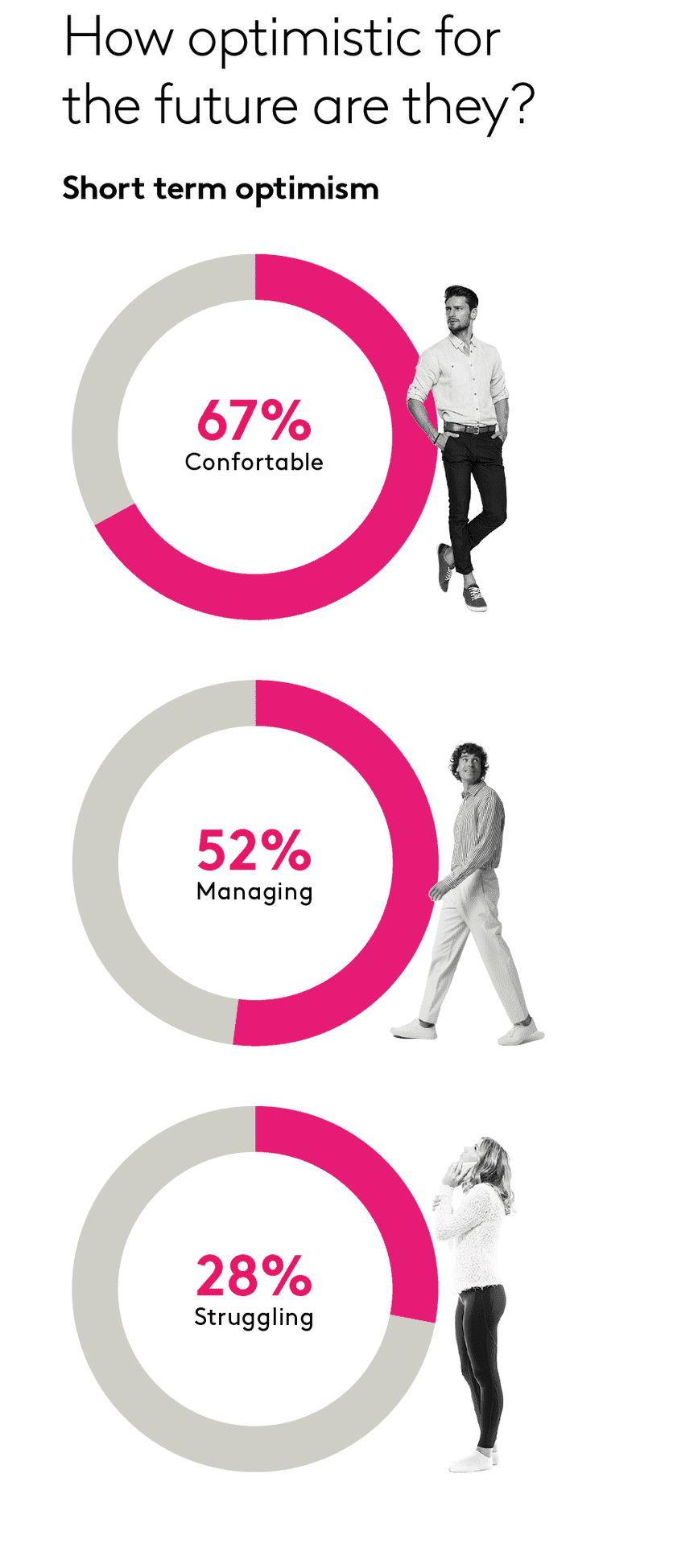

Without doubt, we should expect consumers to be more demanding because they feel much more is being asked of their wallets. Kantar's ongoing examination of households through a lens of three pressure groups – the "comfortable", "managing", and "struggling" – provide critical insights for brands looking to adapt.

Financial faultlines

"Comfortable" households have a mostly relaxed view on spending, enjoying a sense of financial security. The "managing" group is under some strain but remains capable of balancing their budgets, albeit carefully. The "struggling" cohort, on the other hand, experiences severe economic pressures that significantly limit their spending power.

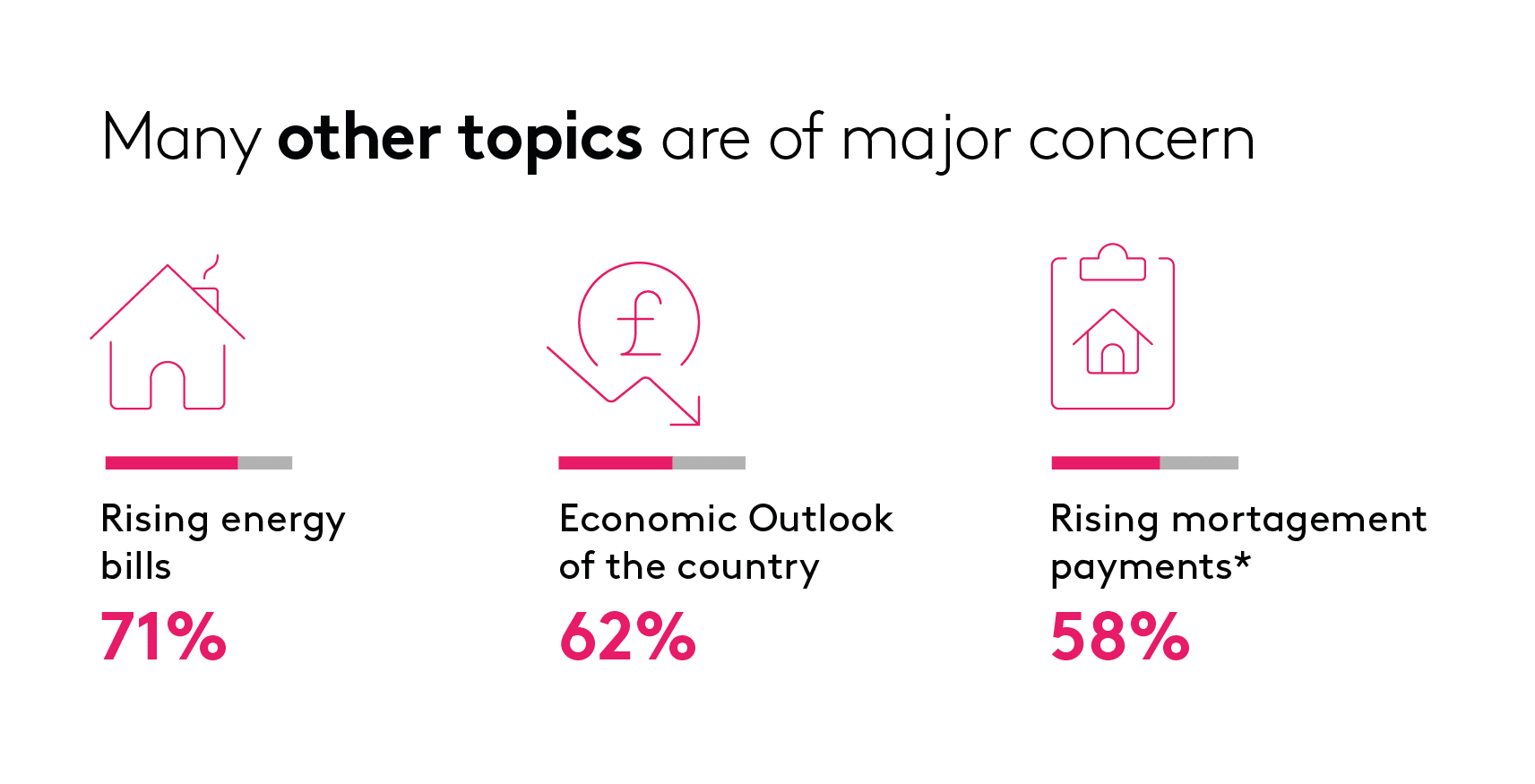

Unsurprisingly, the financial strain for many extends beyond the supermarket aisles. We saw almost unanimous concern from struggling households regarding rising energy costs. This level of apprehension will be important to account for in planning as we head into the winter months. And in a big picture reminder of the challenging times, our pressure group survey shows widespread concerns on rising mortgage and rental costs, even among those in the more comfortable group.

These evolving consumer sentiments underscore a critical need for brands to revisit their strategies. As the economic landscape continues to shift, the opportunity lies in aligning offerings with these changing consumer needs. In doing so, brands have a chance to connect more deeply with consumers desperate for lifelines.

Growth is possible

Understanding and responding to these needs will be crucial if existing customers are to be retained and new ones recruited. In other words, there is room to succeed for those who make room to do so. Those already succeeding are redefining their value proposition and building stronger connections with consumers.

And they’re doing it despite intensified competition from own-label products and broader price pressures. There are still areas such as toiletries, alcohol, and household items where branded innovation growth remains strong. The market is still ripe for consumer goods brands to distinguish themselves and attract consumer attention.

To seize growth opportunities amidst these challenges, there are (at least) two key areas that FMCG brands and retailers should focus on relentlessly:

1 · They need to adapt their product offerings to cater to the full range of consumer groups, perhaps offering more own-label products in specific categories while persisting in branded innovation in others.

2 · It's not just about price; brands and retailers must explore different types of value to offer consumers. This could entail improved packaging, transparency on supply chain and product sourcing, or added product benefits. Brands also need to improve their communication regarding the value they offer and be more transparent about their pricing. This will reassure price-sensitive consumers and reduce their risk perceptions during the purchasing decision.

Interestingly, the top New Product Developments (NPDs) in 2022 found ways to appeal to the increasing number of struggling households. Seven out of the top 10 products in Britain over-indexed with the group who identified to Kantar as struggling. The managing group, on the other hand, tended to gravitate towards what could be considered upgrades from the basics to premium or premium-feel food and drink products. As you’ll see in our report, Madri beer, Britain's top NPD of the year, was a popular choice among this group.

However, getting the product alone right is not enough; brands must also pay attention to its presentation and marketing. Innovative packaging that enhances the product experience and provides added value can also create a sense of excitement and anticipation around the product and help build an emotional connection with consumers.

This strategy, as illustrated by the success of Madri and others, could be instrumental in retaining and attracting customers amidst a challenging economic landscape.