The Global Top 50

The most chosen FMCG brands in the world

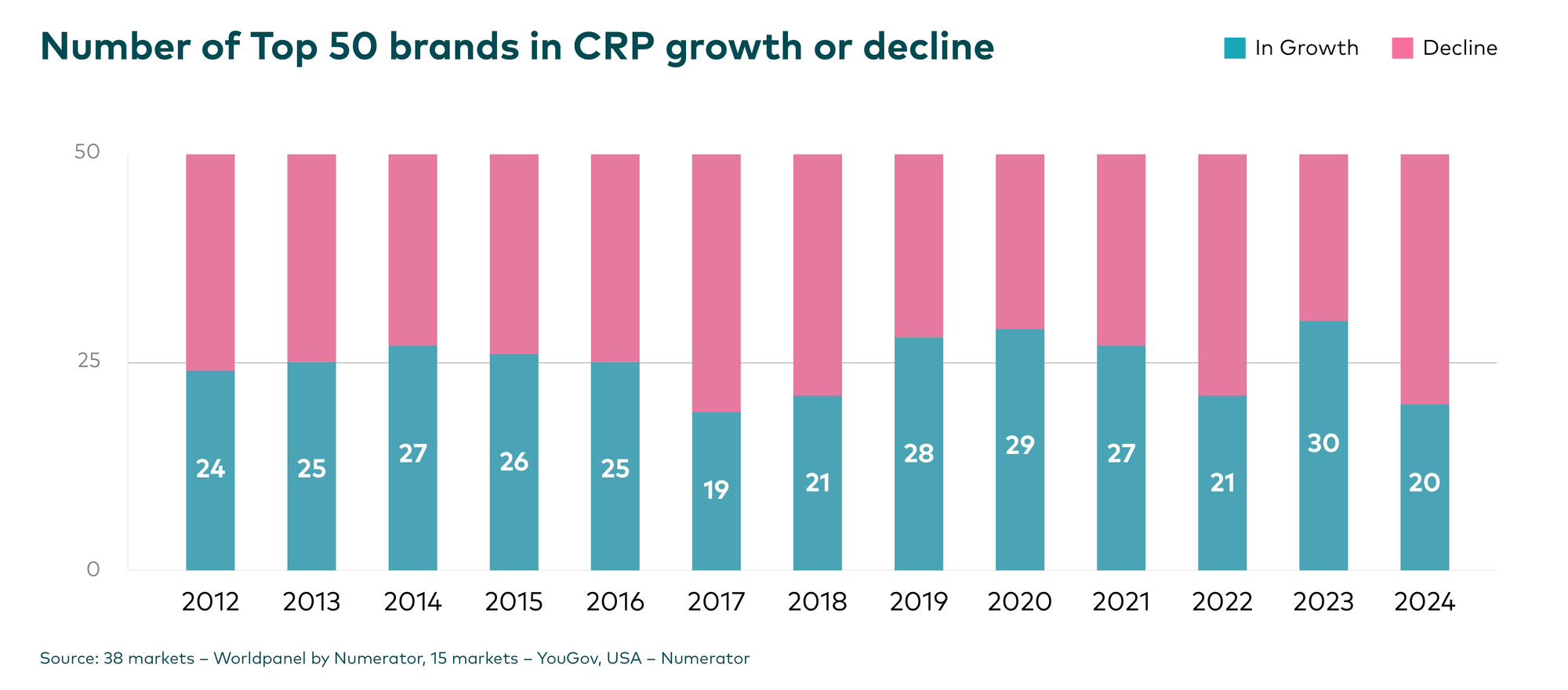

Before unveiling this year's Brand Footprint Top 50, it’s worth re-emphasising that the 50:50 game has consistently applied to the global brands in our ranking since 2012. The average number of brands in growth over the 13 editions stands at 25 – bang on 50%.

However, in 2024, just 20 of the global Top 50 were growing – quite a reduction from 2023’s record high of 30 brands.

That's the nature of the 50:50 game: some years swing one way, others swing back, but the underlying principle remains constant. And when analysing 50 brands rather than tens of thousands the swings look more dramatic.

While this topline view paints a more negative picture than in previous years, digging a bit further into the numbers provides a reality check: the Top 50 were still chosen a combined 88 billion times in 2024, just a 0.6% reduction from 2023. These 50 giants are being chosen only slightly less often, with the 20 growing brands’ Consumer Reach Point (CRP) gains almost offsetting the losses made by the 30 in decline.

However this still represents a shift; so what is driving it? The simple answer lies in India's influence on global brand performance. In 2024, we observed a slowdown in FMCG industry growth in this crucial market, with the total rise in CRPs dropping from 8% in 2023 to 5% in 2024.

This directly impacted the Global Top 50. Of the brands in the ranking with a strong Indian presence, 82% grew their CRPs in 2023. Fast forward a year and this number fell to 68%. Put another way: of the brands that declined in India, 100% saw a drop in their total global CRPs.

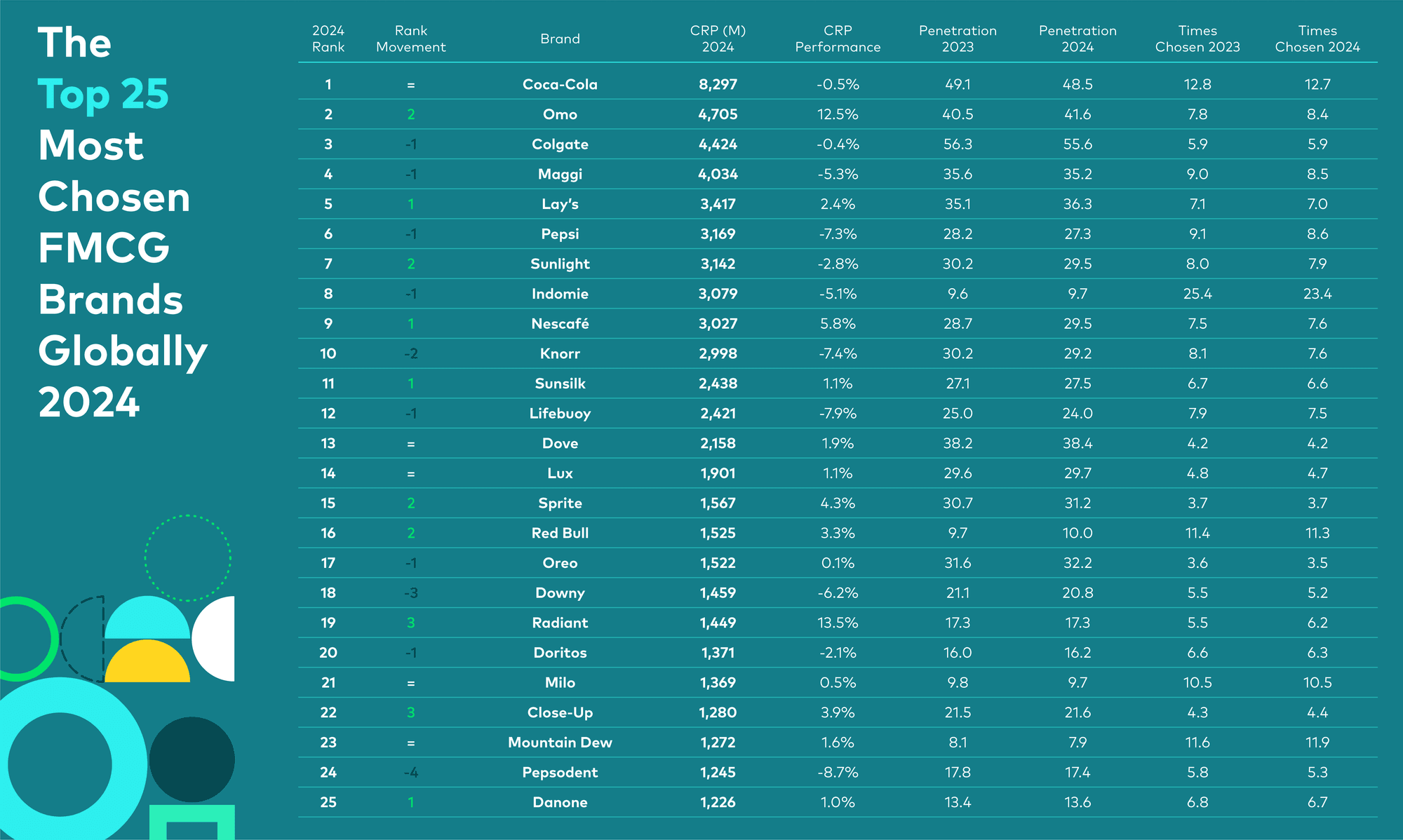

Against this backdrop, here are the Top 50 most chosen brands in 2024.

The headlines from this year's Top 50 Most Chosen Brands reveal a fascinating divide.

Fourteen of the 20 growing brands sit within the Top 25, showcasing the continued resilience of the biggest global brands, while only six from the next 25 saw growth.

OMO saw the biggest increase in CRPs, chosen 4.7 billion times in 2024 – an increase of 520 million – catapulting it to our new number 2 in the global ranking.

Lay's was another high achiever, increasing its CRPs by over 80 million to move up to fifth in the ranking. This signifies eight years of back-to-back growth – a masterclass in momentum.

Nescafé gained over 160 million CRPs, representing quite the turnaround for the brand. Having managed to break the decline momentum, the brand has now achieved four consecutive years of CRP growth.

Dove, with a modest 1.9% rise in CRPs, remains the only brand to have grown in every edition of Brand Footprint – the ultimate consistency champion.

Sprite and Red Bull continue to impress with 4.3% and 3.3% CRP growth respectively. Both were also big winners in the previous two years’ rankings.

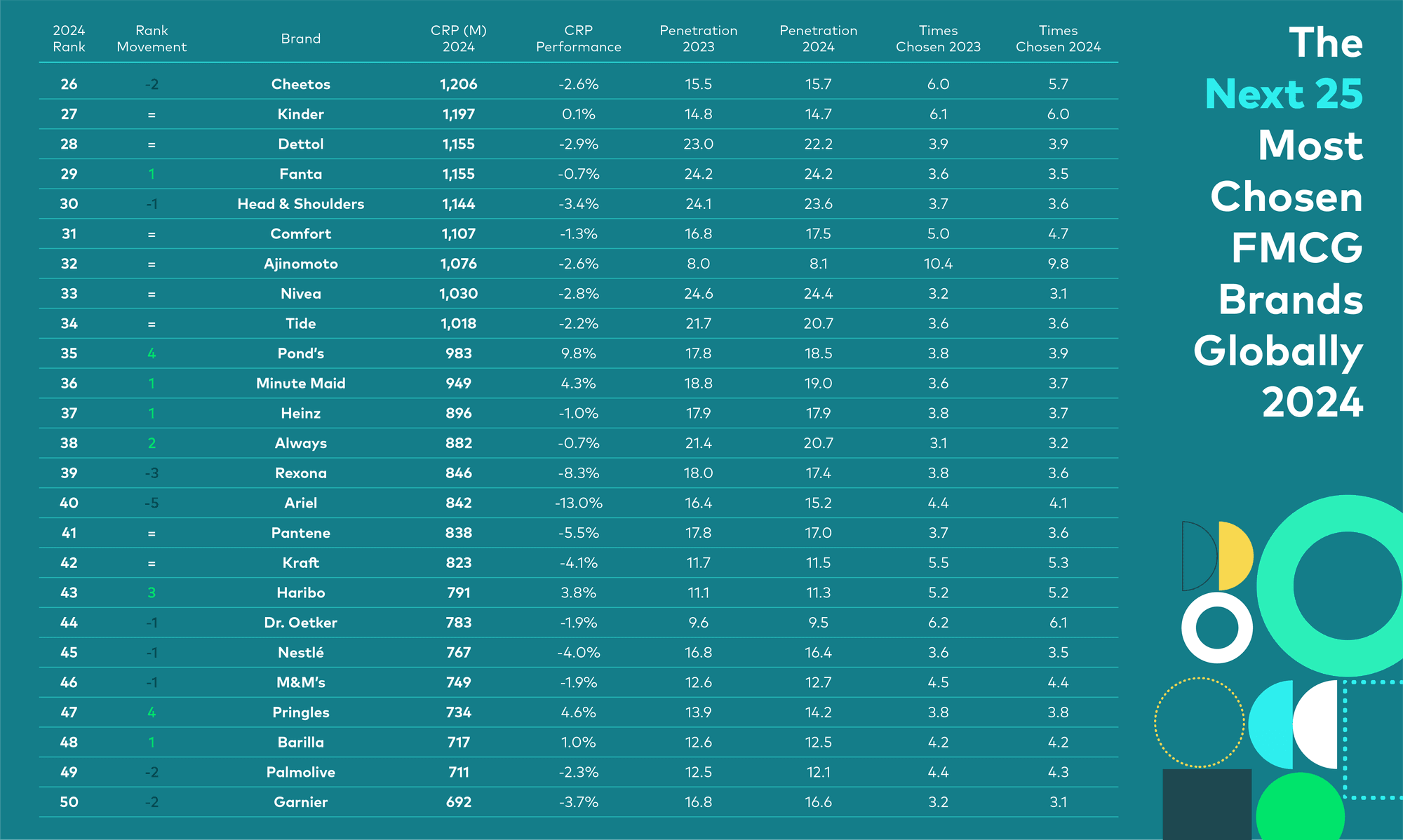

Despite only six brands from the second half of the Top 50 seeing growth, three in particular deserve special recognition:

Pond's rose four places to number 35, adding 88 million CRPs with one of 2024’s biggest global penetration gains.

Haribo cemented its place in the global Top 50, rising three places and adding 29 million CRPs.

Pringles moved from outside the Top 50 to 47th position, adding 32 million CRPs through one of the biggest penetration increases seen last year.

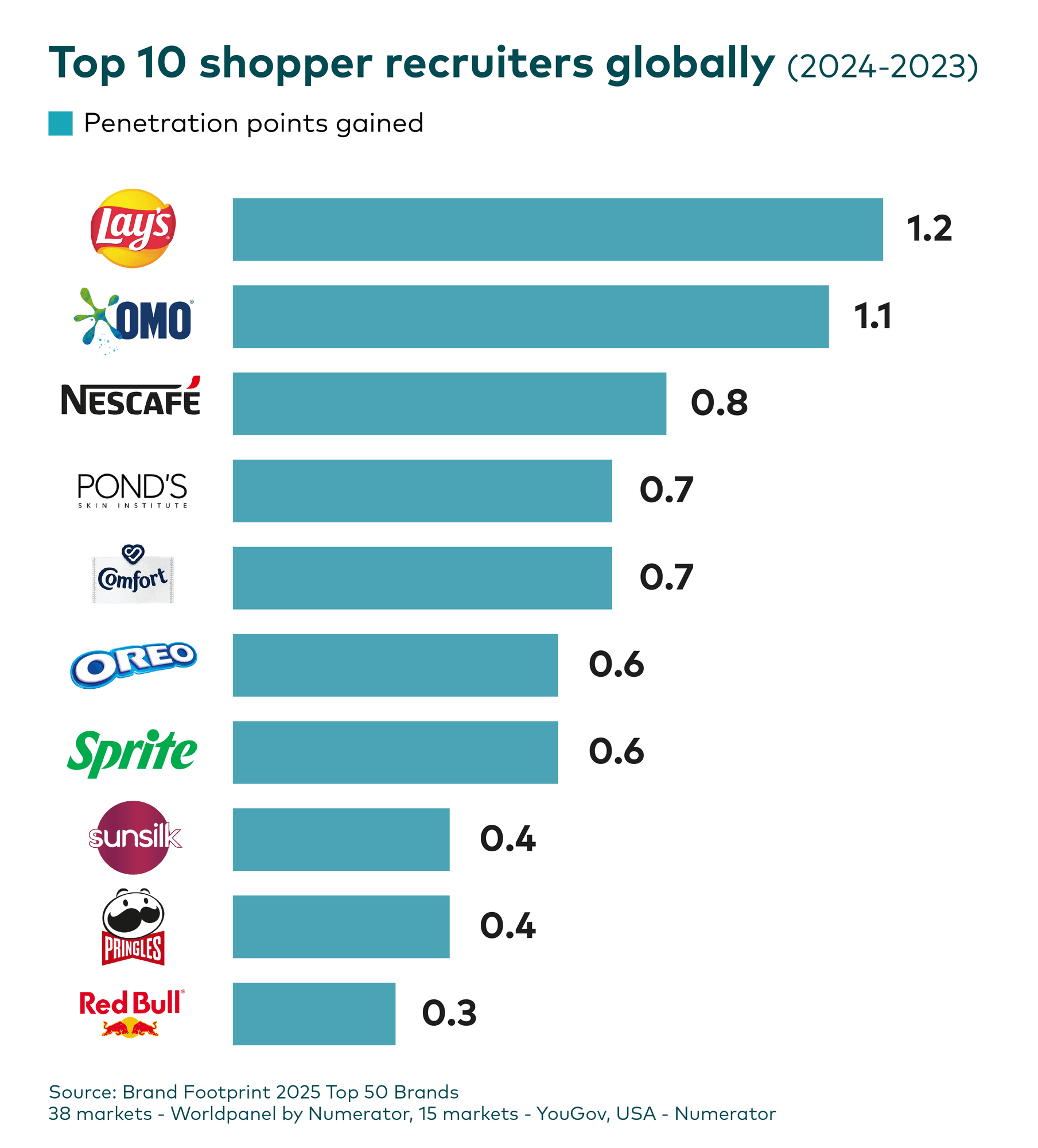

It should come as no surprise that the brands which recruited the most shoppers showcased some of the strongest growth. All of the names appearing on this list deserve congratulations.

The fact that seven of these brands were also top recruiters globally in 2023 demonstrates how powerful momentum truly is. As we showed in the previous chapter, momentum is a powerful force in brand performance and is just as relevant at the global level.

But the brands that really stood out in 2024 were Lay's and OMO, both extending their penetration by over 1% across the globe. This represents an increase in their shopper base of over 20 million shoppers each.

But how exactly did OMO and Lay's achieve these remarkable results? The following chapter reveals the precise strategies that shifted the 50:50 odds decisively in their favour.