Brand resilience in a high-pressure environment

2023

The rankings of the Most Resilient Brands

Thirsty for more?

Larger brands face growth struggles, but can smaller brands make the difference?

Households fight price hikes differently worldwide. Custom strategies needed for every nation.

Post-Covid market sees Own Label and discounters rally. Strong brands must brace for battle.

Regardless of affluence, households buy fewer items and opt for cheaper. Similar path, different scales.

A masterful mix of global reach with a splash of dominance in high-population markets is key.

Predicting growth based on size and position is a gamble. More factors are at play in the growth roulette.

Some countries offer fertile grounds for new buyers amid the cost crisis. India and Bangladesh stand out.

Brands winning globally, like Starbucks and Red Bull, forecast a bright future.

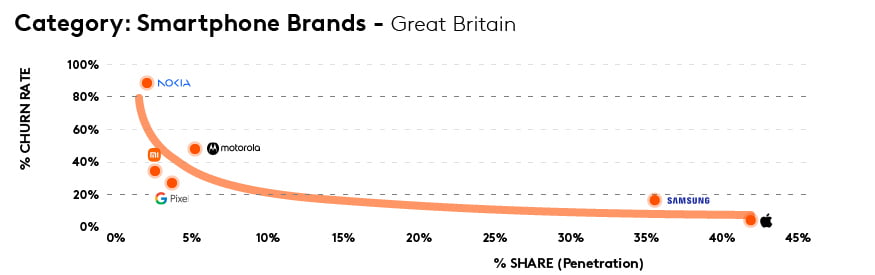

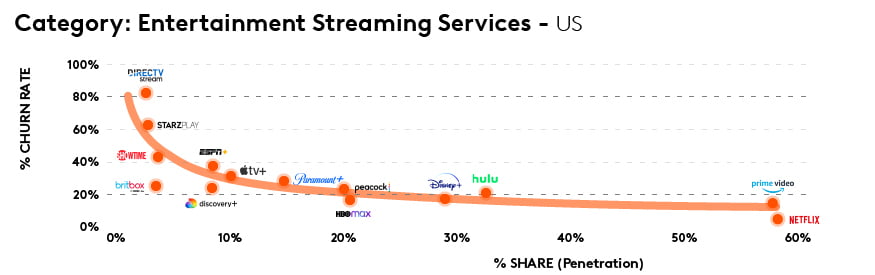

Not just a CPG rule but a cross-industry pattern. Subscription entertainment channels and smartphone ownership echo the trend.

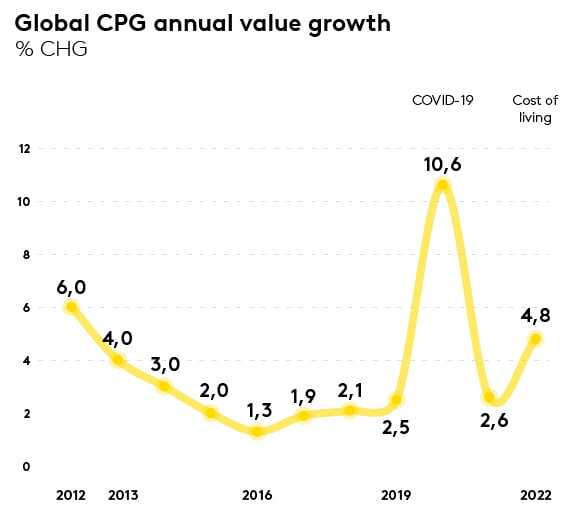

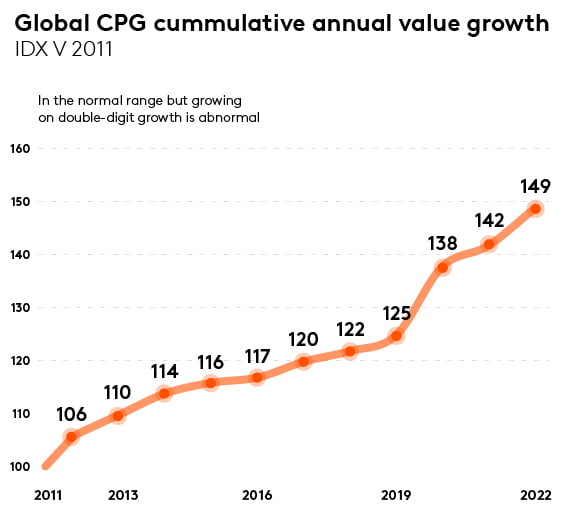

Predicting the post-pandemic paradigm CPG’s return to ‘normal’ growth

The Consumer Packaged Goods (CPG) sector is pushing towards a return to its ‘normal’ growth patterns. The last decade’s steady quarterly growth in most markets has been turned upside down by monster inflation and the fallout of COVID. Yet, amidst this chaos, a silver lining emerges - a return to the comforting predictability of single-digit growth from 2024. The next chapter in the CPG saga is likely to be one of stability and steadiness, barring surprises.

Source: Worldpanel Division, Kantar, Numerator & GfK (50 markets for 2019 to 2022, 47 markets for 2018, 34 markets 2012 to 2017)

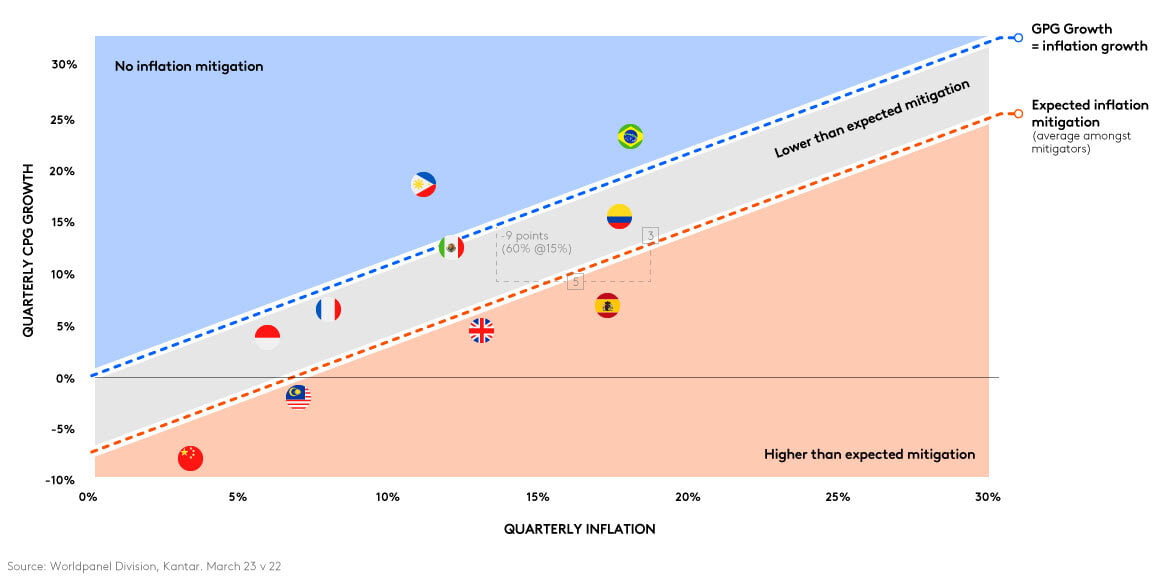

Price rise mitigation is country-specific

As food and grocery inflation hit a staggering 20% in Brazil in Q1 2023, households maneuvered through these surges with minimal visible alterations. While the assumption is households must be trimming other expenses, our data reveals a different narrative. Typically, households combat food and grocery inflation by absorbing the price rise. However, averages can be deceiving. To truly comprehend consumer adaptability, one must delve deeper than mere averages.

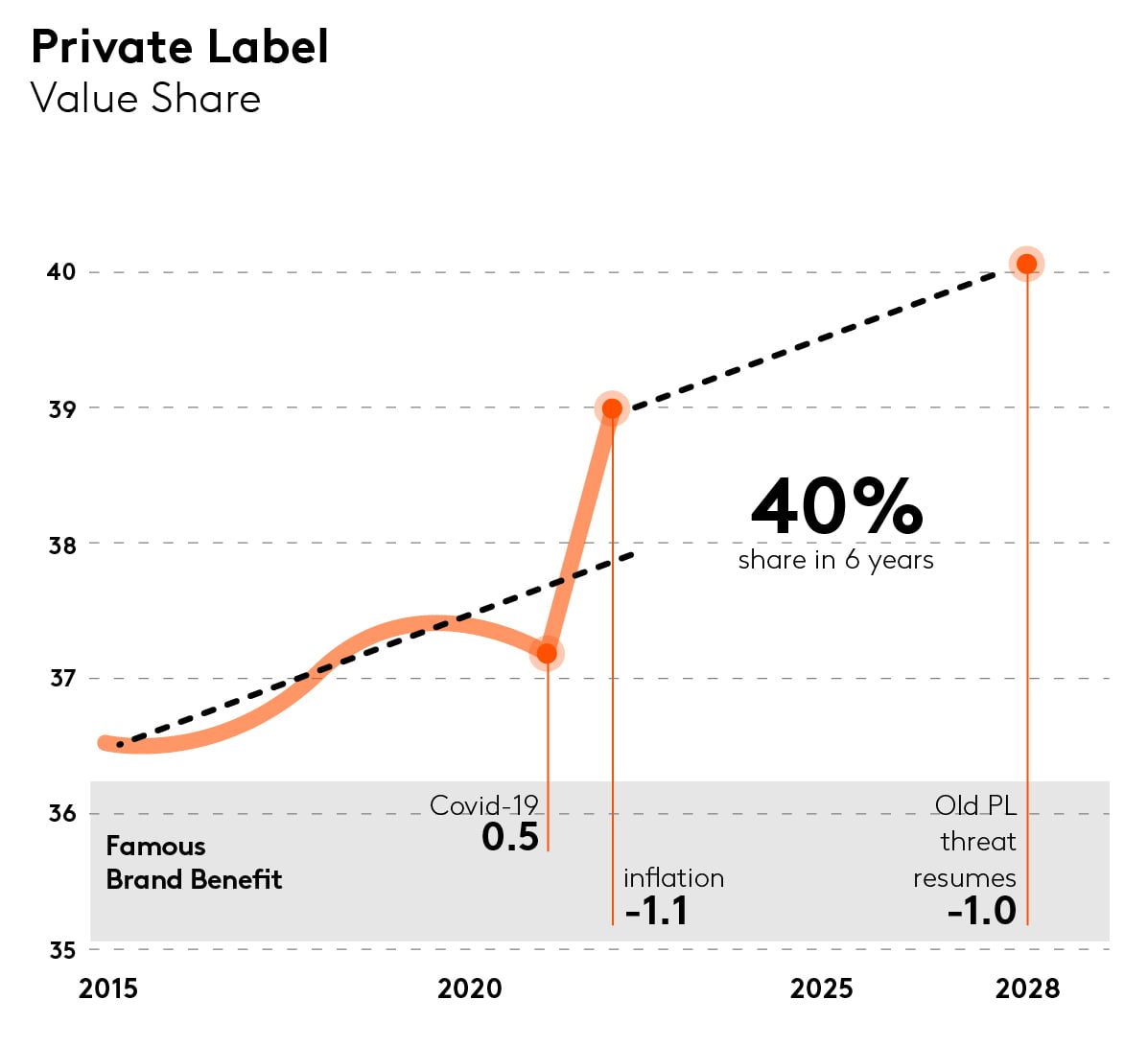

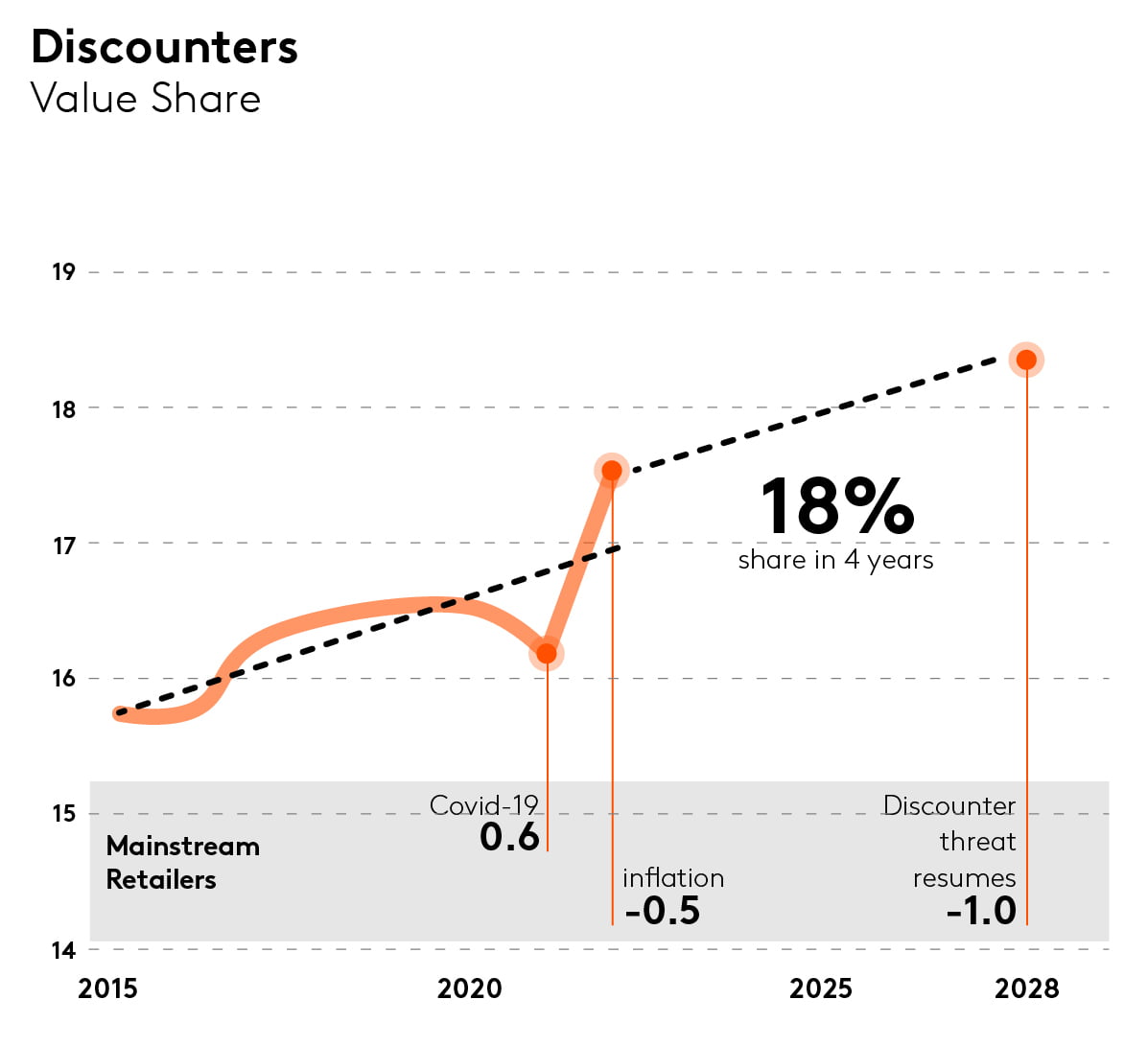

Facing the rise of own labels and discounters

The pandemic stage played in favor of famous brands, with e-commerce trends sidelining discounters. But with the curtain call of the cost-of-living crisis, that spotlight quickly shifted. In a quick turnaround, own labels and discounters soared to their highest market share positions. Looking ahead, we’re likely to see a steady climb, echoing the consistent growth since 2015. In this unfolding narrative, only the strongest brands can withstand the tide of value-driven alternatives. Welcome to the era of the name game, where brands face a rising challenge.

Source: Europanel Barometer, Countries: Europe – Big 6 (Germany, France, UK, Spain, Italy , Netherlands)

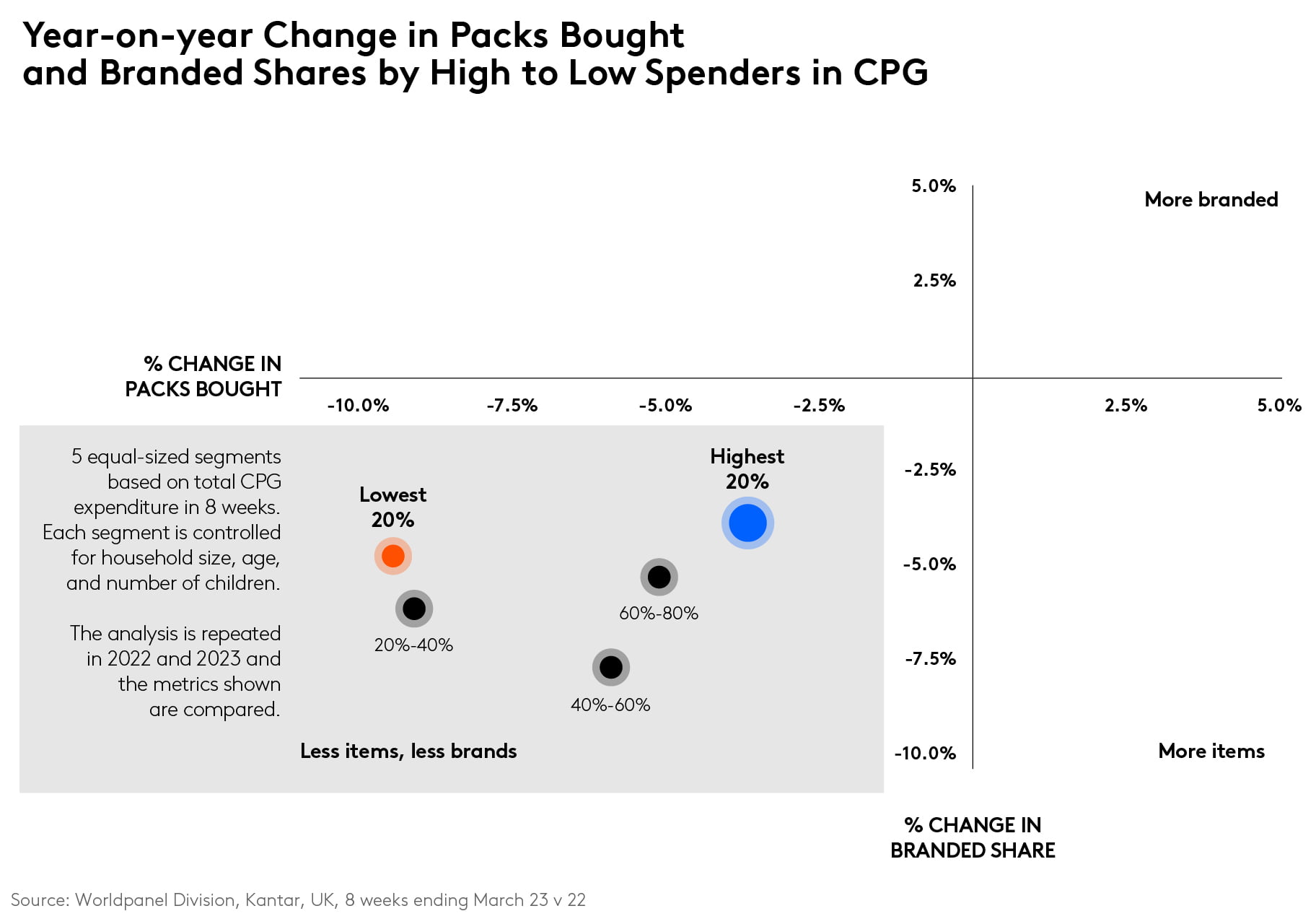

Households cutting back and trading down

Amid rising prices, a unified savings strategy emerges among consumers - both high and low spenders are purchasing fewer packs and gravitating towards budget-friendly alternatives, like own label products. This pattern mimics successful brand marketing tactics, which usually resonate with all buyer types, leading to more purchases and increased frequency.

Low spenders, however, tend to scale back more drastically than their high-spending counterparts, who, while still reducing in relative terms, display the least change - an intriguing behaviour considering their presumed financial comfort.

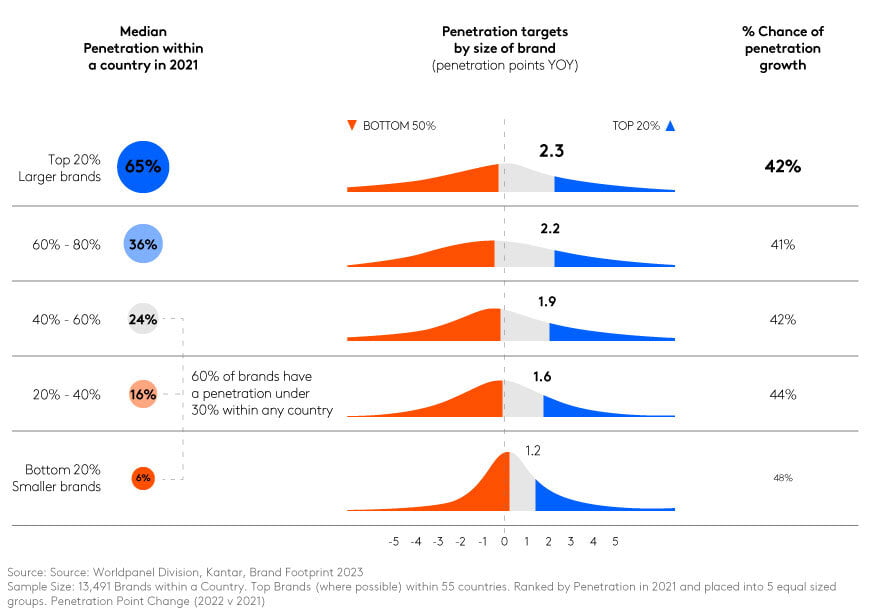

Uphill growth for big players

The brand universe: a complex landscape where giants grapple for growth. Brands securing over 50% of a country’s households yearly fall into the elite 20%, attracting ten times more buyers than the smallest brands. But can these behemoths sustain growth?

The odds are against them. A year of extremity often sees a less extreme follow-up. Smaller brands have a slightly brighter growth prospect but still face likely decline. With larger brands exhibiting more fluctuation, maintaining existing buyers should be a paramount strategy. Defending your stronghold is critical; losses here are challenging to recoup.

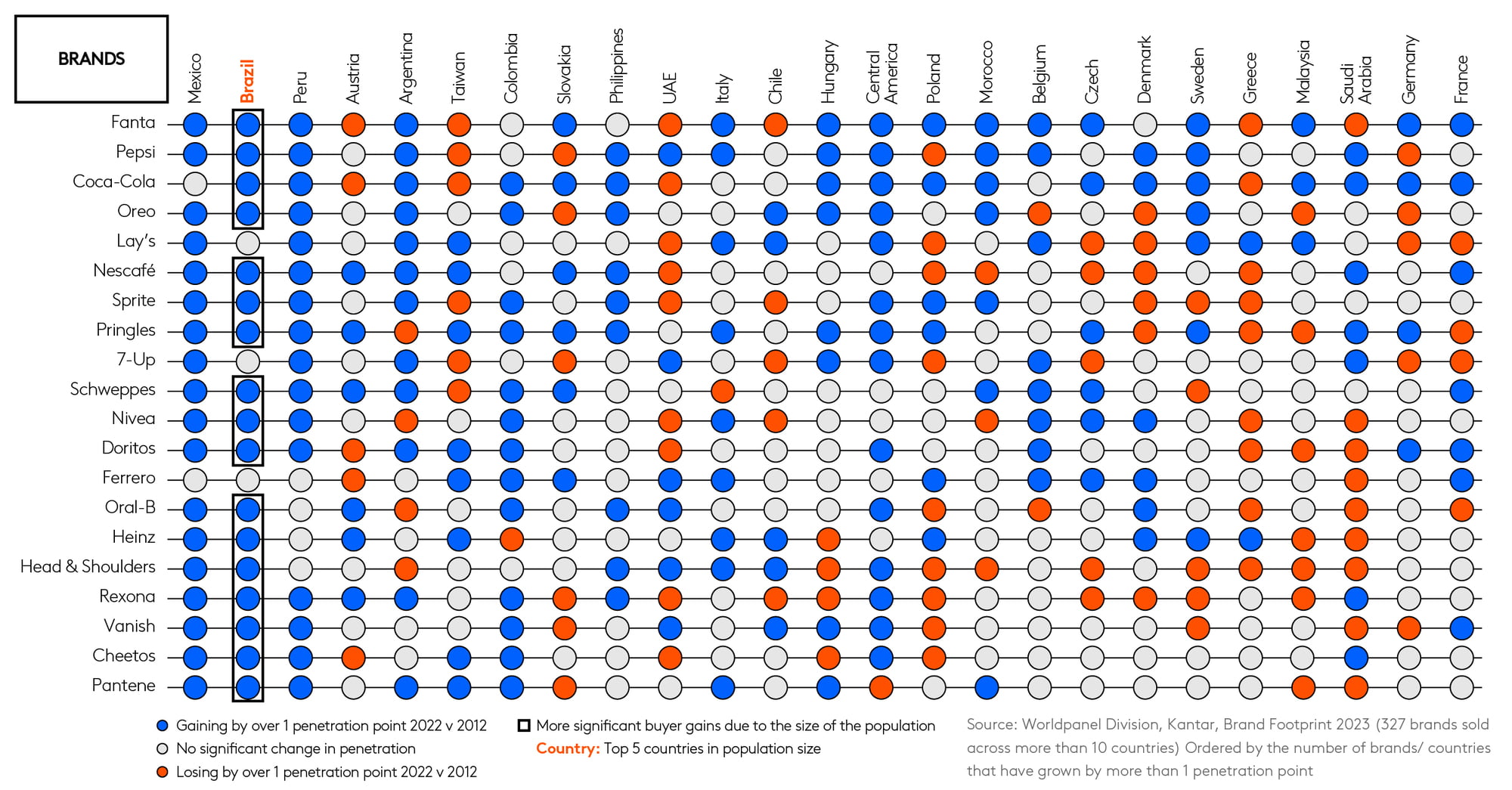

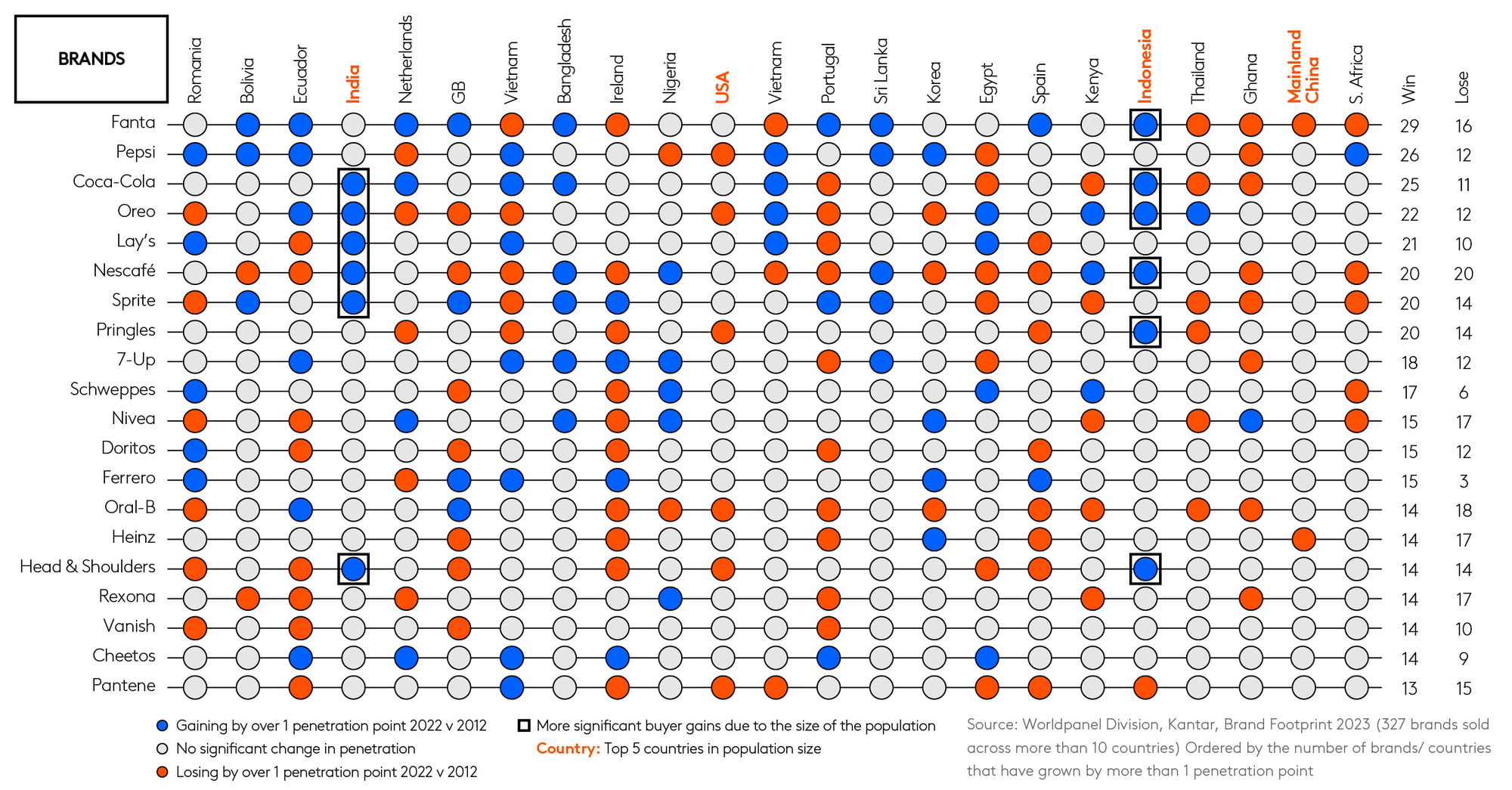

Finding fizz-ical attractions across borders

Capturing new buyers demands a dualfront strategy for brands: cast a wide net globally while ensuring dominance in densely populated markets. Three brands that master this maneuver are Fanta, Pepsi, and Sprite. These beverage titans not only make waves in an array of international territories, but they also command attention and loyalty in populous markets. Their ability to balance geographical expansion with concentrated market penetration serves as a testament to their success and a model for aspiring brands.

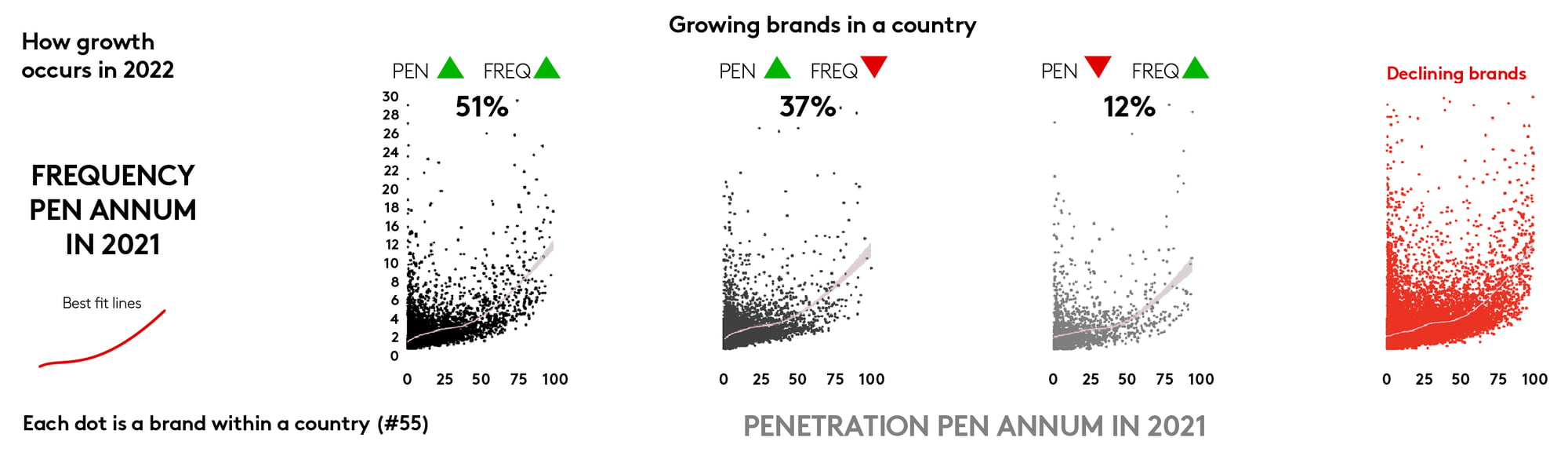

Unravelling brand growth beyond size and position

Penetration - the critical metric of brand growth and the ultimate aim for all brands. Yet, predicting which brands are set to grow, and how, based purely on size and position, becomes a guessing game.The true route to unravelling the penetration puzzle lies in understanding more intricate factors. Current category growth, historical marketing efforts, and trade spending - these elements form the threads we must untangle to truly comprehend brand growth.

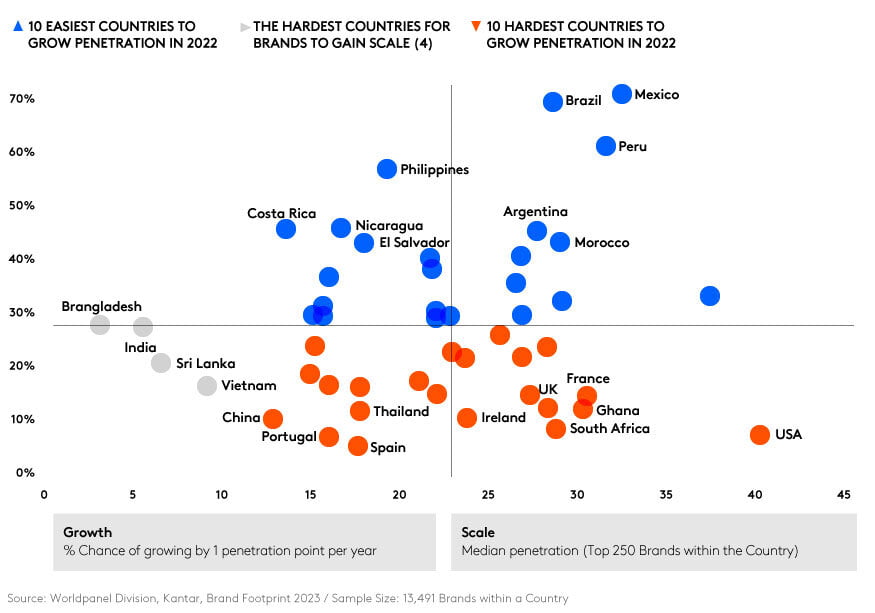

Putting your brand on the map

In the global brand race, geographic location plays a critical role. Using the median annual penetration of the top 250 brands per country, we find the USA leading with a solid 40%. However, untapped potential resides in India and Bangladesh. In the wake of COVID and the unfolding cost-of-living crisis, growth measures provide intriguing insights.

Brands boasting over 1% penetration point growth suggest a country’s potential for expansion. Notably, Mexico and Brazil outshine others, offering seven times more opportunities for winning more buyers than the USA and Spain. Location, indeed, makes all the difference.

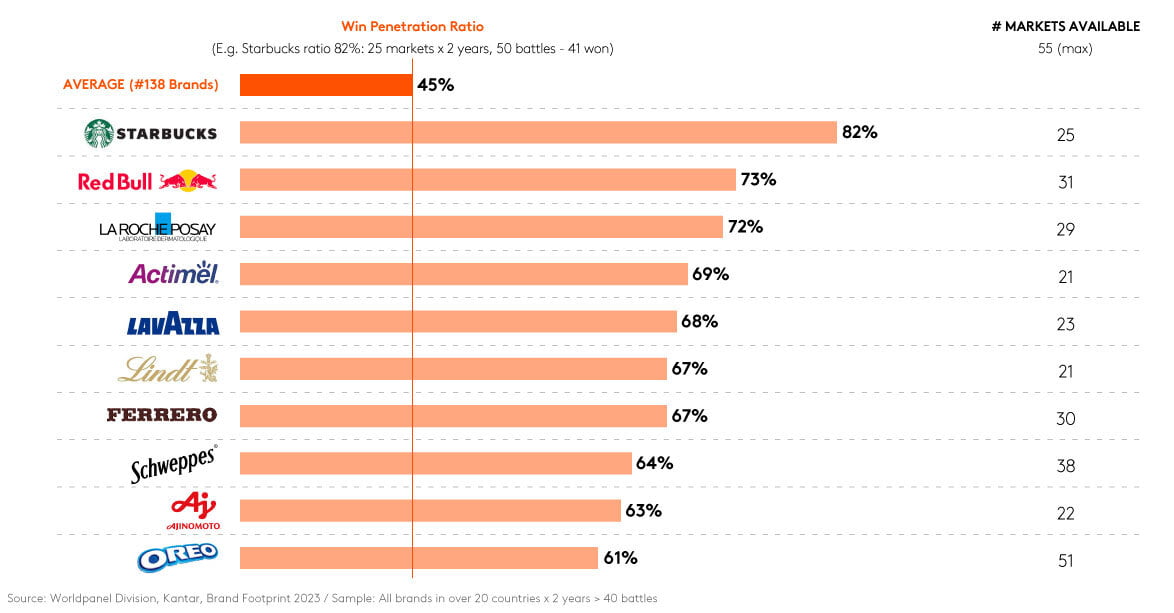

Starbucks sets the brand standard

The hallmark of a robust brand? A growing army of new buyers year after year. A two-year analysis unveils the top 10 brands consistently tipping the scales in their favour. Starbucks emerges as the undeniable champion, nearly doubling the win ratio compared to the average global brand. This caffeinated titan serves as a shining beacon in the world of branding, exemplifying the sweet taste of success through persistent buyer growth. Starbucks isn’t just brewing coffee - it’s steaming ahead in the global brand arena.

Uncovering growth patterns across industries

Brand growth strategies often hinge on the misconception of boosting frequency or spend without expanding the buyer base. But data sings a different tune, upholding the rule of increasing penetration. Yet, many marketers assert their categories are exceptions.

Source: Worldpanel Division, Kantar, ComTech March 2023 (GB), Entertainment on Demand December 2022 (US)

However, the ‘Double Jeopardy’ pattern consistently appears across non-CPG sectors, even in subscription arenas like On-Demand entertainment and for smartphone ownership. Notably, lower subscription and smartphone ownership numbers often coincide with higher churn rates. The principle remains: to lead you must attract more people. By appealing to a broader audience, you also reduce churn among existing customers.